Restructuring the Global Semiconductor Supply Chain: Trends, Challenges, and Opportunities

Metric | Value/Estimate |

|---|---|

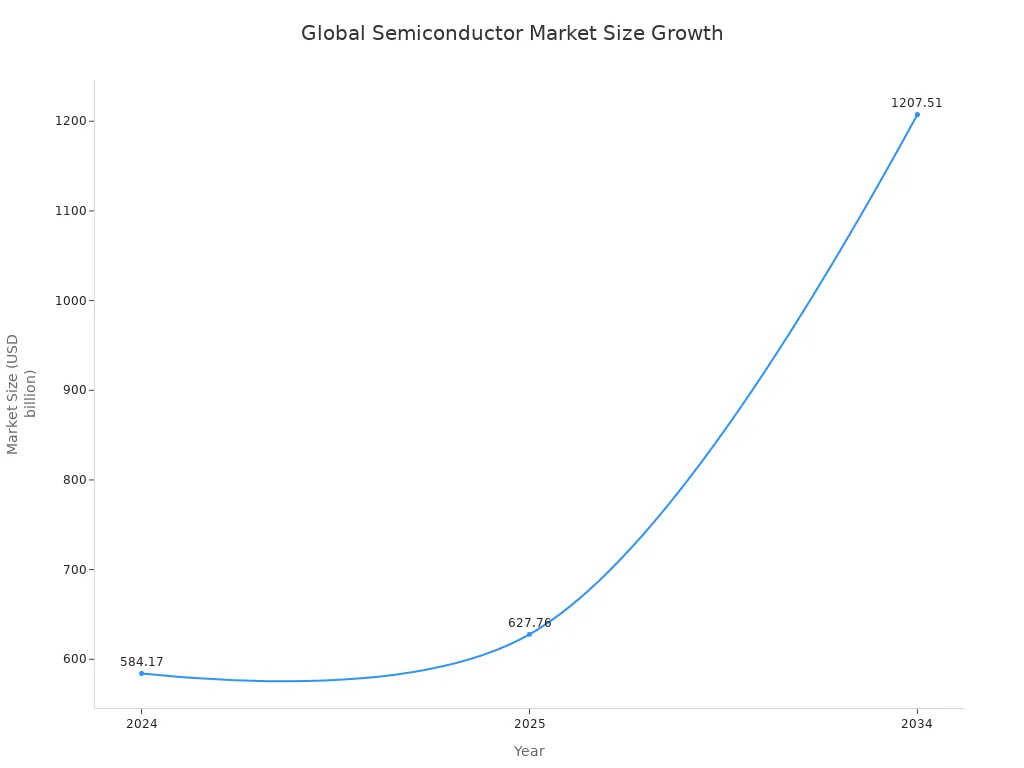

Market Size (2025) | Approx. USD 627.76B |

Market Size (2034) | USD 1,207.51B |

CAGR (2025-2034) | 7.54% |

Largest Market Region | Asia Pacific |

The Global Semiconductor Supply Chain faces major changes as rapid market growth collides with geopolitical tensions and persistent shortages. Lead times peaked at 26.5 weeks in 2022, and over 60% of chips come from Taiwan, making the industry vulnerable. Companies now invest in new capacity and domestic production to build resilience and reduce risks.

Key Takeaways

The global semiconductor supply chain is complex and relies heavily on a few countries, especially Taiwan, making it vulnerable to disruptions.

Geopolitical tensions and natural disasters create risks that companies and governments address by investing in domestic production and reshoring.

Sustainability and technology innovation, like AI and flexible manufacturing, help improve efficiency and reduce environmental impact.

The industry faces challenges such as supply shortages, a growing talent gap, material access risks, and increasing security threats.

Building resilience requires diversification of suppliers, strategic partnerships, digital tools, and strong government support through policies and incentives.

Global Semiconductor Supply Chain Overview

Key Players

The Global Semiconductor Supply Chain relies on a network of countries and companies, each specializing in different segments. Taiwan leads semiconductor capital expenditure, holding 31% of global investment from 2024 to 2032. The United States follows closely with 28%, reflecting its push to expand domestic production. Japan, South Korea, and the Netherlands also play critical roles in manufacturing and equipment supply.

Segment | Leading Countries | Leading Companies (Country) | Market Share / Notes |

|---|---|---|---|

Silicon Wafer Production | Japan, South Korea, Taiwan | SUMCO (Japan), Shin-Etsu Chemical (Japan), SK Siltron (SK) | Japan dominates wafer production |

Silicon Wafer Processing | Japan, South Korea, Taiwan | TSMC (Taiwan), Samsung Electronics (SK), SK Hynix (SK) | Taiwan’s TSMC leads wafer processing |

Photoresist Manufacturing | Japan, South Korea | Tokyo Ohka Kogyo (Japan), JSR Corporation (Japan) | Japan leads photoresist manufacturing |

Etching Chemicals Production | Japan, South Korea, United States | JSR Corporation (Japan), Dow Chemical (USA), Air Liquide (France) | Japan and USA lead etching chemicals |

Doping Chemicals Production | United States, Japan, Germany | Dow Chemical (USA), BASF (Germany), Honeywell (USA) | USA and Japan lead doping chemicals |

Semiconductor Packaging | Taiwan, China, South Korea | ASE Group (Taiwan), Amkor Technology (USA) | Taiwan leads packaging |

Semiconductor Testing | United States, Japan, South Korea | Keysight Technologies (USA), Advantest (Japan) | USA and Japan lead testing |

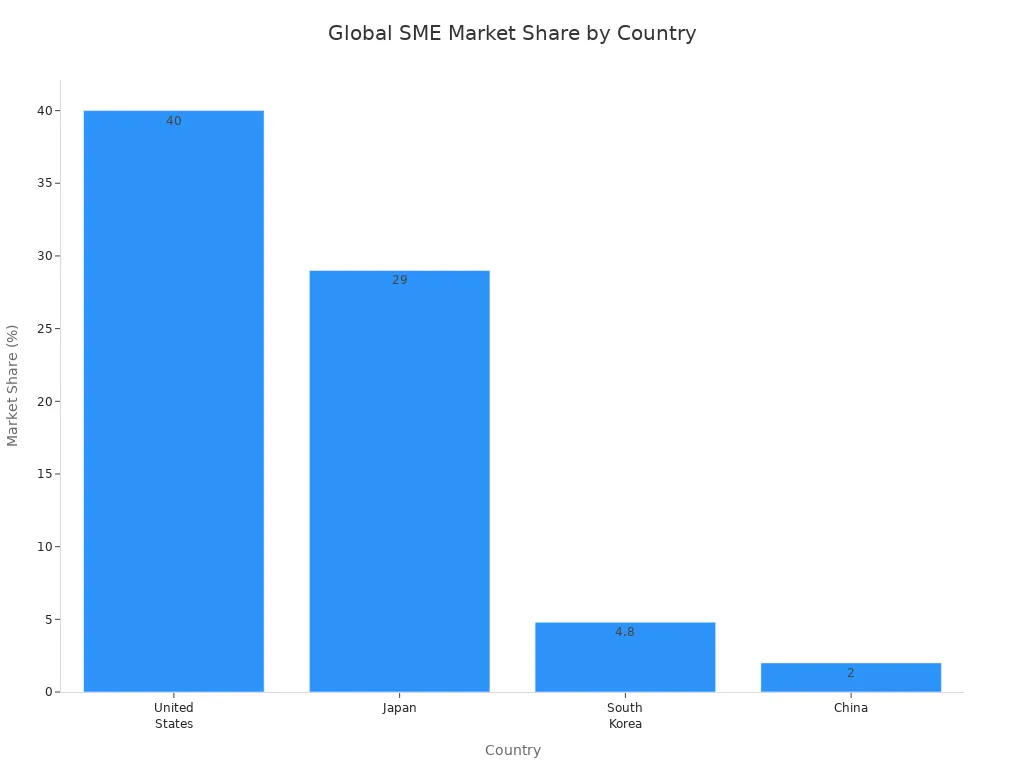

Semiconductor Manufacturing Equipment (SME) | United States, Japan, South Korea, China | Applied Materials, Lam Research, KLA Tencor (USA), ASML (Netherlands), Nikon, Canon (Japan) | US holds >40% SME market share, Japan 29%, South Korea 4.8%, China <2% |

Semiconductor Capital Expenditure (2024-2032) | Taiwan, United States | N/A | Taiwan leads with 31%, US second with 28% |

Wafer Fab Equipment (WFE) | United States, Japan, Netherlands | Applied Materials, Lam Research, KLA Tencor (USA), ASML (Netherlands), Nikon, Canon (Japan) | US holds 44% global WFE market share; Japan second largest supplier; ASML sole EUV provider |

Assembly, Test, Packaging Equipment | United States, Japan, Netherlands | Various US and Japanese firms | US firms >40% SME market share; Japan 29%; South Korea 4.8%; China <2% |

Complexity and Vulnerabilities

The Global Semiconductor Supply Chain faces many challenges due to its structure and global reach. Several factors add to its complexity and vulnerability:

Geopolitical tensions, such as US-China trade disputes and export controls, disrupt supply and create uncertainty.

Natural disasters, including earthquakes and floods, threaten fabrication sites. For example, the 2011 earthquake in Japan and recent events in Taiwan have caused major disruptions.

The supply chain involves many specialized steps—design, fabrication, assembly, testing, and packaging—spread across a few regions. This concentration increases risk.

Taiwan produces 60% of chips and 90% of advanced semiconductors, making it a single point of failure.

Multiple disruptions, like the COVID-19 pandemic and severe weather, can combine to prolong instability.

Note: Climate change, rising costs, and cyber risks also threaten the supply chain. Droughts in Taiwan have affected water supplies needed for chip production. Cyber-attacks and economic pressures add further risk.

The Global Semiconductor Supply Chain remains vulnerable to both natural and human-made disruptions. Companies and governments must address these risks to ensure a stable supply of semiconductors.

Trends

Geopolitical Shifts

Geopolitical events have reshaped the Global Semiconductor Supply Chain in recent years. Several major developments have influenced the industry:

The U.S. CHIPS Act encourages domestic semiconductor production and restricts China’s access to advanced manufacturing equipment. This move highlights the growing competition between the U.S. and China.

Taiwan, through TSMC, produces over half of the world’s chips. Concerns about potential conflict with China have led to new fabrication plants in Arizona and Japan.

The Netherlands’ ASML faces pressure to limit exports of critical lithography equipment to China, reflecting global tensions.

China’s leadership in electric vehicle sales, which depend on semiconductors, increases its influence in the sector.

Europe struggles with limited investment and bureaucratic challenges, despite subsidies, and lags behind the U.S. and Asia in semiconductor manufacturing.

Disruptions in key maritime routes, such as the Suez Canal and Red Sea, have impacted semiconductor logistics.

Climate change and natural disasters, including droughts in Taiwan and typhoons in Malaysia, have caused operational bottlenecks.

The U.S.-China technology competition has also changed manufacturing and trade flows. The table below summarizes the main impacts:

Aspect | Evidence and Impact |

|---|---|

U.S. Export Controls | Since October 2022, the U.S. imposed strict export controls on advanced semiconductor technology exports to China, especially for chips with military applications. These controls expanded in 2023 and 2024. |

Impact on China | China’s semiconductor ecosystem faced disruptions, price spikes, and workforce reductions. China accelerated efforts for self-reliance and innovation. |

Entity List Expansion | The U.S. expanded its Entity List, blocking many Chinese companies from accessing critical technologies. |

Global Supply Chain Effects | These actions fragmented the semiconductor market and disrupted global supply chains, forcing companies to rethink manufacturing strategies. |

Industry and Innovation Dynamics | Both the U.S. and China increased investments in domestic semiconductor capabilities, reshaping competition. |

Strategic Outlook | Export controls alone are not enough. Comprehensive policies and R&D investments are needed for leadership. |

These shifts have made supply chain resilience, diversification, and national security top priorities for governments and companies.

Localization and Reshoring

Localization and reshoring have become central strategies for strengthening semiconductor supply chains. Between October 2024 and April 2025, semiconductor projects made up about 5% of all reshoring announcements but attracted $102.6 billion in capital investment. This accounted for nearly two-thirds of all foreign capital invested during that period. These investments created over 17,600 new jobs, with major deals involving TSMC, Samsung, and ASML.

Several companies and governments have taken action:

GlobalFoundries invested $16 billion to expand manufacturing and advanced packaging in New York and Vermont. This project received support from the U.S. government and major tech firms.

The CHIPS and Science Act provides billions in incentives to boost domestic production and create jobs.

Industry leaders such as Apple, SpaceX, and Qualcomm support reshoring, highlighting its strategic importance.

TSMC is building a $40 billion fab in Arizona. Intel is expanding in Arizona and Ohio.

The U.S. Department of Commerce awarded $2 billion in CHIPS Act grants in January 2025 to support smaller manufacturers, including a Texas-based firm expanding PCB capacity.

Schweitzer Engineering Laboratories opened a $100 million PCB factory in Idaho to improve supply chain resilience.

Government policies play a key role in these efforts. The table below outlines major incentives:

These policies help offset higher domestic costs and encourage local production. They also address risks exposed by the pandemic and trade disputes.

Sustainability Focus

Sustainability has become a core goal for semiconductor manufacturers. Companies now set ambitious targets for emissions, water use, and waste reduction. For example:

Semiconductor fabs use large amounts of water. TSMC consumes 8.9 million gallons daily, prompting adoption of water recycling and advanced cooling.

Waste generation remains high. Semiconductor Manufacturing International Corporation produced over 58,000 metric tons of hazardous waste in 2022.

Fabs use up to 100 megawatt-hours of energy. The industry aims to reduce energy use per dollar of revenue by 15% by 2024.

Companies use lower-impact chemicals, such as FAN gas mixtures, to reduce global warming potential.

Collaboration with local communities and regulators supports responsible water and waste management.

Sustainability efforts are now part of business models, helping reduce costs and improve environmental impact.

The table below highlights key sustainability goals and how companies measure progress:

Description | Measurement / Reporting Methodology | Example Companies / Targets | |

|---|---|---|---|

Emissions Reduction | Targets aligned with Science Based Targets initiative (SBTi) covering scopes 1, 2, and 3 emissions | Establish baseline emissions; prioritize sources; use abatement technology databases | Onsemi, NXP, Analog Devices, AMD, Wolfspeed; 50% reduction by 2030, net-zero by 2050 |

Water Conservation | Advanced water recycling and cooling to reduce freshwater use and wastewater | Monitor usage; implement recycling; collaborate with communities and regulators | TSMC fab: 8.9M gallons daily; up to 98% reduction achieved |

Waste Reduction and Recycling | Programs to minimize hazardous and solid waste; safer chemical alternatives | Track waste; recycling and pollution prevention programs | SMIC waste data; use of FAN gas mixture |

Energy and Resource Efficiency | Improve energy efficiency; increase renewables; adopt energy management systems | Measure energy use; report per revenue; collaborate with suppliers for efficient designs | 15% energy reduction per revenue by 2024 |

Integration into Business | Sustainability goals in business plans and executive leadership ownership | Use data platforms for reporting and analysis; align with strategy | Broad industry trend |

Technology Innovation

Technology innovation drives efficiency and resilience in the semiconductor supply chain. Recent advances include:

Machine vision, AI, and machine learning enable real-time defect detection and yield improvement, reducing waste and improving quality.

Semiconductor software tools optimize design, simulation, and manufacturing, speeding up prototyping and lowering costs.

New packaging techniques, such as 3D and wafer-level packaging, improve performance, miniaturization, and energy efficiency.

AI-driven design tools and sub-5nm process nodes allow for more powerful, energy-efficient chips and faster time-to-market.

Digital twins at device, process, and equipment levels, combined with generative AI, improve prediction, decision-making, and resilience.

Sustainability initiatives, such as green chemistry and renewable energy, support long-term stability and cost reduction.

Stronger cybersecurity protects data integrity as supply chains become more complex.

Advanced data integration and AI technologies connect manufacturing operations, enabling faster, more informed decisions. This transformation improves predictability, reduces disruptions, and creates new opportunities for sustainability and cost savings.

Note: Co-innovation workshops and integration of enterprise systems with manufacturing operations further support these improvements, making the Global Semiconductor Supply Chain more agile and robust.

Key Challenges

Supply Shortages

Semiconductor supply shortages have become a defining challenge for the industry. Multiple factors drive these shortages:

Surging demand from automotive, electronics, and computing sectors.

COVID-19 pandemic disruptions, including worker shortages, plant shutdowns, and port backlogs.

Long manufacturing cycles for advanced equipment, such as EUV lithography machines, which can take over a year to produce.

Limited production capacity, with a few suppliers dominating the market.

Geopolitical factors, such as export controls, that restrict access to advanced manufacturing equipment.

Extended delivery times for key equipment, now reaching 18-24 months.

Rising equipment costs, with some machines exceeding $150 million.

Delays in production lines for advanced chips at major manufacturers like TSMC and Samsung.

Cause / Impact | Description / Quantitative Data |

|---|---|

Surging Chip Demand | Driven by 5G, AI, autonomous driving, IoT; increased investments in wafer fabs by TSMC, Samsung, Intel |

Long Manufacturing Cycles | Complex production of equipment like EUV lithography machines takes a year or more |

Limited Production Capacity | Dominated by few suppliers (ASML, Tokyo Electron, Applied Materials, Lam Research) with limited growth rate |

Geopolitical Factors | US export controls on China restrict advanced equipment exports, increasing demand elsewhere |

Extended Delivery Times | |

Rising Equipment Costs | ASML’s EUV lithography machines cost over $150 million, prices rising due to demand outstripping supply |

Delayed Production Lines | TSMC and Samsung face delays in 5nm and 3nm production lines |

Industry Impact - Automotive | Production halts at Honda’s Swindon plant; output reductions at VW Group plants |

Technological Innovation Slowdown | Shortages delay mass production of advanced chips (3nm and smaller nodes) |

Competitive Landscape Shift | Larger companies with more resources gain advantage; smaller firms face survival challenges |

Supply shortages have rippled through downstream industries. The automotive sector experienced production halts and backlogs, with estimated global losses reaching $110 billion by May 2021. Chip manufacturers shifted capacity to meet booming consumer electronics demand during the pandemic, leaving automakers with fewer chips. These disruptions highlight the interconnectedness of the Global Semiconductor Supply Chain and the difficulty of quickly resolving shortages. Supply-driven shocks, such as the 2011 Japan earthquake and recent substrate shortages, have proven especially damaging, causing cascading effects across industries.

⚠️ Note: The automotive industry, which relies on both advanced and legacy chips, faces unique challenges due to uneven investment and workforce shortages in semiconductor manufacturing.

Talent Gap

The semiconductor industry faces a significant talent gap that threatens its growth and innovation. The global industry will need over 1 million skilled workers by 2030, requiring the recruitment of 100,000 professionals each year. In the United States alone, a shortfall of 67,000 semiconductor professionals is projected by 2030.

Shortage of STEM graduates and an aging workforce create a "talent cliff."

Negative perceptions of the industry and shifting skill requirements, especially in AI and machine learning, make recruitment difficult.

Semiconductor design engineers are in particularly short supply, with a projected shortage of 23,000 designers if current trends continue.

Specialized skills lacking include digital and analog design, verification, validation, and AI/ML-related architecture expertise.

The talent gap affects engineers, materials scientists, and technicians.

Aspect | Details |

|---|---|

Current Talent Gap | Significant shortage of engineers and technicians |

Projected Engineer Demand | |

Projected Technician Demand | 75,000 new technicians needed annually by 2029 |

Current Supply of Engineers | About 1,500 engineers join the industry annually (3% of engineering grads) |

Current Supply of Technicians | About 1,000 new technicians enter the field annually |

Causes of Talent Gap | Lack of STEM graduates, aging workforce, shifting skill requirements |

Workforce Initiatives | CHIPS Act programs, private sector, and state-level initiatives |

Effectiveness of Initiatives | Engineer gap may persist until 2028; technician shortage may be avoided |

Mitigation Strategies | Workforce planning, reskilling, automation, AI adoption, partnerships |

Projected Talent Gap Range | 59,000 to 146,000 workers short by 2029 |

Additional Notes | Construction labor shortages impact fab expansions |

McKinsey analysis suggests the shortage of semiconductor engineers will worsen until about 2028, even with workforce development programs. Technician shortages may be avoided if training programs meet targets, but the industry must reduce attrition and attract more talent from universities and other sectors. Companies collaborate with public, academic, and private partners to expand the talent pipeline, especially in regions with new fabrication plants. Upskilling technicians and investing in construction labor development remain critical.

Material Access

Material access represents a major vulnerability for the semiconductor industry. China controls about 60% of global rare earth mining and 90% of processing and refining. The United States has no domestic production of 14 critical minerals and relies entirely on imports. This concentration creates strategic risks for the Global Semiconductor Supply Chain.

Key materials at risk include tantalum, silicon, neon, gallium, and process gases such as helium, arsine, krypton, and xenon.

China supplies about 98% of raw gallium and dominates rare earth mining and processing.

Africa and China together supply around 70% of tantalum and silicon.

Neon, essential for photolithography, comes mainly from Russia and Ukraine. The war in Ukraine disrupted about half of the global neon supply.

Export restrictions and sanctions on Russia have further tightened neon availability.

Process gases must be ultra-pure, and their supply is geographically concentrated, increasing vulnerability.

Geopolitical risks, such as trade disputes, export bans, and conflicts, exacerbate supply concentration risks.

Some materials have few alternative sources, making the supply chain fragile.

Manufacturers mitigate these risks by strategic stockpiling of raw materials. However, the lack of alternative sources for many critical inputs means that any disruption can have immediate and widespread effects.

💡 Tip: Companies should diversify suppliers and invest in recycling and alternative material research to reduce dependency on single sources.

Security Risks

Security risks in the semiconductor supply chain have grown more complex and severe. Threats include cyberattacks, physical tampering, and systemic vulnerabilities due to supplier concentration.

CI/CD pipeline attacks, such as the SolarWinds breach, allow attackers to inject malicious code into supplier environments.

Physical infrastructure attacks and hardware backdoors, highlighted by the 2024 Hezbollah supply chain attack, expose hardware to tampering.

Critical supplier concentration means a single compromised supplier can disrupt the entire ecosystem.

Cloud supply chain complexity increases the attack surface, especially with misconfigurations and opaque subcontractor relationships.

Regulatory and geopolitical volatility can abruptly disrupt supplier relationships.

Fragmented incident response plans amplify damage during breaches.

AI-driven social engineering and deepfakes increase the risk of fraud and data theft.

Nation-state actors have increasingly targeted semiconductor supply chains with sophisticated cyber campaigns. In July 2025, a China-backed group infiltrated six Taiwanese semiconductor organizations through tampered software updates, stealing hundreds of gigabytes of sensitive data. Over 60% of breaches start from IT vulnerabilities, such as phishing or VPN exploits. The 2023 ransomware attack on MKS Instruments, a key supplier, disrupted manufacturing workflows across the ecosystem. AI-generated malicious code can embed hardware Trojans during chip design, creating permanent vulnerabilities. Experts recommend mapping dependencies, segmenting IT and operational networks, enforcing multifactor authentication, and hardening third-party access.

🔒 Alert: The evolving threat landscape demands secure development practices, physical security, supplier diversification, regulatory awareness, coordinated incident response, and AI-aware defenses.

Opportunities

New Markets

The semiconductor industry is entering a period of rapid expansion. The global market could reach $2 trillion by 2032, growing at a rate of 15.4% each year. Asia Pacific leads this growth, holding over half of the market share in 2024. Countries like India, Vietnam, Israel, and Singapore are becoming important players. India’s market reached $30 billion in 2023 and is growing fast due to government support and strong local demand. Vietnam attracts foreign investment with low costs and new infrastructure. Israel’s tech ecosystem and Singapore’s advanced facilities also drive growth.

Emerging Market | 2023/2025 Market Size | Projected Growth | Key Drivers |

|---|---|---|---|

India | $30B (2023) | 17% CAGR | Incentives, demand, partnerships |

Vietnam | N/A | 10% CAGR | Investments, incentives, upgrades |

Israel | N/A | 12% annual | Tech, venture capital, innovation |

Singapore | $49.06B (2025) | 8% CAGR | Location, infrastructure, major firms |

🌏 Companies should explore partnerships and investments in these regions to capture new demand and diversify their supply chains.

Policy Support

Governments play a key role in shaping the semiconductor industry. The U.S. CHIPS Act and similar programs worldwide provide funding, tax credits, and grants. For example, the U.S. Department of the Treasury funds the Semiconductor Growth Access Program to help small businesses in New York. Colorado’s CHIPS Community Support grants target new markets and rural areas. Since 2020, over 130 projects in 28 states have attracted more than $600 billion in private investment. These policies create jobs, boost research, and strengthen supply chains.

Companies should monitor new policy incentives and apply for grants to support expansion.

Collaboration with local governments can unlock additional resources and support.

Strategic Partnerships

Strategic partnerships drive innovation and resilience. Tesla and Samsung work together on chips for self-driving cars. The U.S. and EU coordinate research through organizations like imec and NSTC. In 2024, Apollo invested $11 billion in Intel’s Fab 34, and NXP joined Vanguard International Semiconductor to build a new fab in Singapore.

Firms should seek alliances that combine technology, capital, and market access.

Cross-border partnerships can help companies share risks and accelerate product development.

Digitalization

Digital tools are transforming supply chain management. Companies use AI, machine learning, and IoT to monitor production and predict demand. Big data analytics improve quality control and reduce delays. Blockchain and digital twins increase transparency and security. These technologies help companies respond quickly to disruptions and optimize operations.

Investing in digital skills and infrastructure can boost efficiency and resilience.

Stakeholders should adopt real-time data systems to improve decision-making and collaboration.

💡 Embracing digitalization and strategic partnerships, while leveraging policy support and new markets, will help companies thrive in the evolving semiconductor landscape.

Industry leaders face rapid change and disruption. They invest in new technologies, diversify suppliers, and expand into emerging markets. Analysts recommend these strategies for future success:

Collaborate across production, sales, and R&D.

Focus on customized solutions and efficient fulfillment.

Aspect | Stakeholder View |

|---|---|

Geographic concentration, overspecialization | |

Opportunities | Policy innovation, flexible design |

Companies must balance risk and opportunity. Will they build a smarter, more resilient supply chain for tomorrow’s challenges?

FAQ

What causes most disruptions in the semiconductor supply chain?

Natural disasters, geopolitical tensions, and supply concentration create most disruptions. Companies face risks from earthquakes, trade disputes, and reliance on a few suppliers. These factors can stop production and delay shipments.

How do companies improve supply chain resilience?

Companies diversify suppliers, invest in flexible manufacturing, and use digital tools. They also map their supply networks and build strong relationships with partners. These steps help reduce risks and respond quickly to problems.

Why is talent important in semiconductor manufacturing?

Skilled workers design, build, and maintain advanced chips. The industry needs engineers, technicians, and scientists. A talent gap slows innovation and limits production. Companies invest in training and partnerships to attract new talent.

See Also

Enhancing Supply Chain Performance In Advanced Manufacturing Industries

Addressing Supply Chain Growth Problems Amid Globalization Trends

Collaborative Innovation To Strengthen Supplier Bonds In Manufacturing

Expert Advice For Overcoming Automotive Supply Chain Obstacles