Semiconductor Supply Chain Futures: Growth Pathways, Innovation, Security Resilience, and Worldwide Trends

The semiconductor supply chain faces urgent challenges as global demand surges. In 2024, the market reached $627.6 billion, marking a 19.1% increase from 2023.

Metric | Value (2024) | Projected Growth (CAGR) |

|---|---|---|

Global Semiconductor Market Size | 15.4% CAGR (2025-2032 forecast) |

Major investments, including the CHIPS Act’s $52.7 billion commitment, drive new capacity and innovation. Companies must build resilience and adapt to shifting global trends.

Key Takeaways

The semiconductor market is growing fast, driven by AI, automotive tech, and government investments like the CHIPS Act.

Innovation in chip design and manufacturing, including AI tools and new materials, boosts performance and efficiency.

Regional diversification and local investments reduce risks from geopolitical tensions and supply chain disruptions.

Cybersecurity and risk management are critical to protect the supply chain from attacks and ensure steady production.

Talent shortages challenge the industry, but training programs and partnerships help build a skilled workforce for the future.

Growth Pathways

Market Drivers

The semiconductor industry in 2024 shows strong momentum. Sales reached $627.6 billion, a 19.1% increase from the previous year. Major investments, such as the $450 billion in global capacity expansion and the U.S. CHIPS Act, fuel this growth. Several key factors drive the market forward:

Resurgent demand and government incentives power global fab investments. The industry plans to open 82 new volume fabs in 2024, boosting wafer production capacity by 13% year-on-year.

Artificial intelligence (AI), high-performance computing (HPC), and 5G technologies create new opportunities. AI and HPC drive memory sector growth, with DRAM capacity rising by 5%.

Automotive electrification and computerization increase demand for discrete and analog components. Discrete capacity grows by 7%, and analog by 10% in 2024.

Automotive remains the top revenue driver. Cars now require between 1,000 and 3,500 chips each, especially for electric and autonomous vehicles.

Wireless communications, cloud/data centers, and IoT also contribute to market expansion.

Microprocessors, including GPUs for AI, represent the top product growth opportunity.

Government incentives and strategic investments support capacity expansion and innovation.

Most industry executives expect continued revenue growth in 2024.

AI integration accelerates semiconductor demand. Modular AI chiplets improve performance, reduce costs, and enable tailored solutions for workloads like autonomous driving and HPC. These chiplets combine multiple functions, optimize power, and allow faster development. The automotive sector increases semiconductor needs as vehicles become software-defined and autonomous. Connectivity features in cars require high-speed data processing and real-time communication. AI chips play a vital role in sensors, CPUs, and predictive analytics, driving complexity and volume.

The industry expects to reach $1 trillion by the end of the decade. AI, HPC, automotive electrification, and connectivity technologies lead this growth. The automotive semiconductor market is projected to grow at a 10% compound annual rate from 2024 to 2030. Custom accelerators and integrated circuits optimized for energy efficiency and security become critical for specialized AI workloads. AI also helps optimize semiconductor manufacturing, improving quality and speeding up time-to-market.

Emerging Applications

New applications continue to shape the future of semiconductors. The industry sees rapid growth in several areas:

AI demands advanced chips for high-speed processing, driving innovation.

Cloud infrastructure expansion increases the need for efficient and robust semiconductor supply chains.

Consumer electronics, including smartphones and wearables, require more powerful and energy-efficient chips.

Automotive applications, especially electric vehicles and autonomous driving, create new opportunities for chips that meet safety and performance standards.

AI processors and custom processing units (XPUs) are expected to drive significant growth, especially in data centers.

Data centers, servers, and storage markets are projected to grow rapidly, with semiconductor sales increasing by 2030.

High-bandwidth memory demand surged by 200% in 2024, driven by AI and cloud computing.

The automotive sector, including electric and autonomous vehicles, benefits semiconductor foundries.

The solid-state drive (SSD) market is projected to grow at a 17.6% CAGR, reflecting increased demand in cloud and automotive sectors.

New materials such as graphene and other two-dimensional materials are being integrated with silicon to overcome miniaturization limits and enhance device functionality.

Compound semiconductors like gallium nitride and gallium arsenide offer superior performance for power electronics, RF communications, and photonics.

Chiplet technology enables modular, specialized semiconductor components to be integrated efficiently, improving production yields and enabling smaller, more advanced devices.

Innovations such as 3D transistors, gate-all-around (GAA) architectures, and new memory technologies support these emerging applications. The industry also explores flexible electronics, magnetoelectric spin-orbit logic devices, and advanced packaging solutions like Intel’s Embedded Multidie Interconnect Bridge (EMIB). These advances help meet the growing complexity and performance needs of next-generation devices.

Regional Investment

Regional investment shapes the semiconductor landscape. Governments and companies invest heavily to boost local production, innovation, and supply chain resilience.

Region | Key Investments and Initiatives | Market Size / Forecast | Focus Areas and Drivers |

|---|---|---|---|

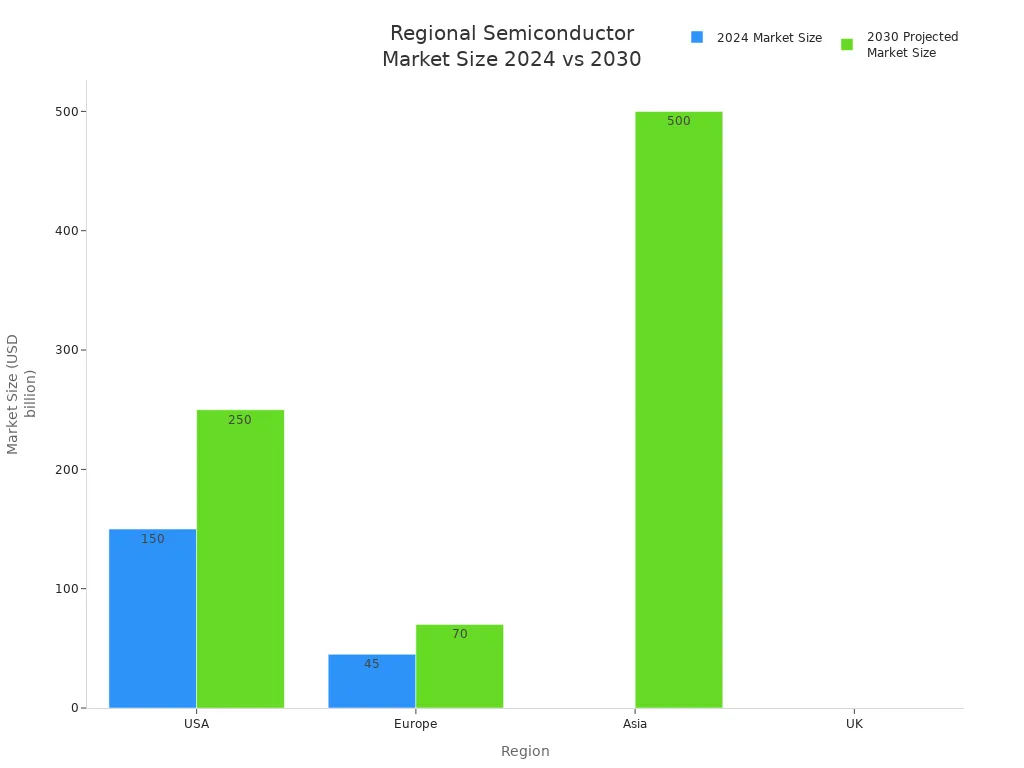

USA | CHIPS for America Act promoting domestic manufacturing and innovation; investments by Intel, NVIDIA, Qualcomm; focus on next-gen tech like quantum computing and memristive computing | $150 billion in 2024, projected $250 billion by 2030 (7.5% CAGR) | AI, cloud computing, 5G, autonomous vehicles; addressing supply chain resilience |

Europe | €43 billion Western Chips Act aiming to double semiconductor production by 2030; emphasis on digital sovereignty and local production | $45 billion in 2024, projected $70 billion by 2030 (6.5% CAGR) | Automotive (EVs, intelligent driving), Industry 4.0, IoT, AI, quantum computing |

Asia | Massive investments by China, Taiwan, South Korea, Japan; focus on production capacity and advanced technologies; China reducing reliance on foreign tech | Projected $500 billion by 2030 (9% CAGR) | Consumer electronics, 5G, IoT, AI, healthcare, finance, autonomous vehicles; supply chain robustness |

UK | Investments in AI and advanced manufacturing; government innovation hubs; National AI and Digital Strategies | Forecasted £5 billion market size by 2025 (7% CAGR) | AI, telecommunications, healthcare, EVs, autonomous driving, 5G, energy-efficient semiconductors |

Geographic diversification strengthens growth and resilience. Companies shift investments away from China, with 40% redirecting to Southeast Asia. Over 70% of U.S. firms with manufacturing in China plan to move operations to other countries. Firms adopt "Taiwan+1" strategies to reduce concentration risk. Governments in the U.S., EU, Japan, South Korea, Australia, and India implement "right-shoring" policies to reduce reliance on single regions. Incentives such as subsidies, tax credits, and talent development programs attract semiconductor manufacturing investments domestically and regionally.

East Asia holds over 75% of global semiconductor manufacturing, creating vulnerability to geopolitical and natural disruptions. The U.S. CHIPS and Science Act allocates $52.7 billion to boost domestic production, aiming to increase the U.S. share from 10% to 14% by 2032. The European CHIPS Act targets doubling EU capacity to 20% of the global market by 2030. Emerging hubs like Southeast Asia and India gain importance due to cost advantages and government incentives. Companies adopt multi-sourcing strategies and form global partnerships to reduce single-source dependency. Investments in workforce development, advanced technologies, and supply chain transparency support diversification and resilience.

Note: Regional investment and geographic diversification are essential for building a robust and secure semiconductor supply chain. These strategies help mitigate risks and ensure continued growth in a rapidly changing global market.

Innovation

Advanced Manufacturing

Semiconductor manufacturing has entered a new era. Companies now use extreme ultraviolet (EUV) lithography with high numerical aperture (NA) and multi-patterning to create chips at sub-2nm nodes. This technology improves resolution and increases production speed. The industry has shifted from FinFET to gate-all-around (GAA) transistors, which offer better control and reduce power loss. Manufacturers like TSMC, Intel, and AMD use 3D packaging and chiplet architectures to boost performance and scalability. New materials, such as graphene and gallium nitride, help chips run faster and cooler. AI-driven design and manufacturing tools optimize chip layouts, predict equipment failures, and improve quality. Companies also focus on energy-efficient manufacturing and recycling to lower environmental impact.

Note: The expansion of fabs in the US and Japan, along with efforts to diversify production, strengthens supply chain security and reduces risks from global disruptions.

Chip Design

Chip design has become smarter and faster. AI now automates many design steps, such as layout generation, logic synthesis, and defect detection. This reduces errors and speeds up development. Leading companies use AI-powered tools to inspect wafers, control processes, and predict maintenance needs. These tools improve yield and cut waste. Advanced memory technologies, like high-bandwidth memory, and new cooling systems, such as liquid cooling for GPUs, support high-performance computing. Modular chiplet designs and AI-optimized memory placement help meet the demands of AI and data center applications. FPGAs and neuromorphic chips also play a key role in flexible, energy-efficient designs.

Sustainability Challenges

The semiconductor industry faces major sustainability challenges:

High energy use and greenhouse gas emissions from manufacturing.

Large amounts of water and chemicals needed for chip production.

Ethical concerns over sourcing rare materials like cobalt and palladium.

Regional differences in environmental regulations.

Companies invest in renewable energy, water recycling, and green chemistry. However, the push for sustainability can conflict with security and market dominance. Reliable power is critical for chip production. Shifting to renewable energy or diversifying supply chains may introduce risks or disrupt operations. For example, Taiwan’s efforts to increase renewable energy face delays, which could threaten global chip supplies. The industry must balance environmental goals with the need for stable, secure, and competitive manufacturing.

Semiconductor Supply Chain Security

Geopolitical Risks

Geopolitical risks present major challenges for the semiconductor supply chain. The US-China trade war has led to tariffs and export controls, which increase costs and restrict the flow of technology. Taiwan stands as a critical hub for semiconductor manufacturing. Threats against Taiwan could cause catastrophic losses, with estimates reaching $490 billion in annual revenue for electronic device manufacturers. The supply chain remains highly concentrated in regions like Taiwan, China, the US, and South Korea. This concentration creates vulnerabilities to conflicts and export restrictions.

Onshoring semiconductor production is complex and expensive. Building a single factory can cost at least $10 billion and take five years to complete. Labor shortages in technical roles also threaten expansion plans. Governments and companies now explore friend-shoring strategies, which involve working with trusted partners to reduce risks. Safeguarding Taiwan’s security is essential for global stability. Disruptions in the semiconductor supply chain have broad economic impacts. During the COVID-19 pandemic, shortages affected 169 industries and caused $210 billion in lost automotive revenues.

Recent global events, such as trade disputes and regional conflicts, have stressed the semiconductor supply chain. These risks disrupt the flow of materials and products, leading to shortages and increased volatility. Governments respond with initiatives like the U.S. CHIPS Act and the European Chips Act. These policies promote domestic manufacturing and aim to reduce dependency on foreign suppliers.

Note: The semiconductor supply chain relies on politically unstable regions for raw materials and monopolistic suppliers for critical equipment. Building resilience through domestic manufacturing is costly and time-consuming. Companies must proactively manage vulnerabilities, as they have better visibility into operational risks than governments.

Cybersecurity

Cybersecurity threats continue to grow within the semiconductor supply chain. Attackers often target weaker third-party vendors and suppliers, bypassing direct defenses. Phishing remains the primary initial attack vector, responsible for over 90% of incidents. Vulnerabilities in open-source software components introduce security blind spots. State-sponsored threat actors conduct espionage campaigns focused on intellectual property theft. Employment-themed phishing emails with malware increase infection rates.

Nation-state actors embed persistent access into software pipelines and fabrication operations to steal intellectual property. Taiwan’s semiconductor industry is a prime target due to its strategic importance. IT-OT convergence creates new attack vectors, with over 60% of breaches starting from IT vulnerabilities like phishing. Supply chain compromises can cascade, as seen in ransomware attacks disrupting multiple suppliers. AI-generated malicious code can embed hardware Trojans during chip design, creating permanent vulnerabilities.

Cybercriminals target weak links such as embedded systems, third-party vendors, legacy tooling, and industrial infrastructure. Insider threats, corrupted firmware, tampering, and data exfiltration via vendor software updates are major concerns. Smaller subcontractors and logistics partners often lack adequate security controls, serving as soft targets. Visibility into Tier 2 and Tier 3 suppliers is limited, increasing risk within the supply chain.

The semiconductor industry addresses these threats through collective action. Manufacturers, equipment vendors, and software providers work together. Key initiatives include the SEMI E187 fab equipment cybersecurity specification, which sets baseline security requirements for suppliers. The Semiconductor Manufacturing Cybersecurity Consortium (SMCC) focuses on enhancing cyber resilience across the supply chain. These efforts aim to standardize assessments, reduce supplier burden, and align with global regulations.

Semiconductor companies integrate AI with existing ERP, MES, and SCM systems to improve supply chain efficiency while ensuring cybersecurity. Successful AI implementation requires robust cybersecurity measures to address data privacy, legacy system integration, and change management. Leading manufacturers like Intel, TSMC, Samsung, Qualcomm, and NVIDIA leverage AI supported by strong cybersecurity practices to optimize supply chain operations. Talent development and collaboration with ecosystem partners are critical to sustaining secure AI-driven supply chain transformations.

Risk Mitigation

Companies adopt comprehensive risk mitigation strategies to address vulnerabilities in the semiconductor supply chain.

Diversification of supply sources reduces dependency on single suppliers. Companies multi-source from different vendors and regions, regionalize production facilities, and nearshore or reshore production closer to key markets.

Building strategic reserves helps buffer against disruptions. Companies maintain inventories and safety stocks, and form partnerships for shared inventory management.

Strengthening supplier relationships fosters stability. Long-term collaboration, open communication, and joint innovation ensure access to cutting-edge technology.

Investing in advanced technologies enhances visibility and operational efficiency. AI, machine learning, blockchain, automation, IoT, and Industry 4.0 tools allow proactive disruption management.

Prioritizing sustainability supports long-term resilience. Circular economy principles, renewable energy use, and sustainable sourcing reduce environmental impact.

Supplier risk analysis enables companies to systematically identify, assess, and mitigate risks before disruptions occur. This proactive approach maintains supply chain visibility and helps avoid costly production shutdowns.

Government policies frame semiconductor supply chains as critical to national security. The concentration of advanced manufacturing in Taiwan creates a geopolitical risk that governments must manage. The US and its allies recognize that dispersed global supply chains pose vulnerabilities when suppliers are in sensitive regions. Policies now incentivize geographic diversification and strengthen domestic and allied manufacturing capabilities. Regulations control technology transfer and restrict movement of equipment to adversarial nations. Public-private and international partnerships enhance resilience and manage intellectual property with security considerations.

Tip: Companies should map dependencies, segment IT-OT pathways, enforce multifactor authentication, and harden third-party access. Collaboration among industry, academia, and government agencies builds a robust cybersecurity ecosystem.

Worldwide Trends

Regional Diversification

Regional diversification shapes the future of the Semiconductor Supply Chain. Governments invest heavily to promote innovation and self-reliance. The U.S. CHIPS Act and Europe’s Chips Act drive domestic manufacturing and reduce reliance on East Asia. India emerges as a new player with the India Semiconductor Mission and major company investments. Mexico and Vietnam grow as alternative hubs for manufacturing and assembly. Companies diversify suppliers and invest in domestic supply chains to enhance resilience. Advanced technologies like AI and market intelligence improve supply chain management. Collaboration with knowledgeable distributors supports stability.

Aspect | Evidence Summary |

|---|---|

Regional Dominance | Taiwan, South Korea, and China lead wafer fabrication; China controls rare earths, Japan photoresists, EU specialty gases. |

Government Initiatives | U.S. CHIPS Act and Europe’s Chips Act boost domestic manufacturing and reduce reliance on East Asia. |

Emerging Hubs | Mexico and Vietnam expand as nearshoring hubs; India gains attention but remains in early stages. |

Risks and Challenges | Geopolitical tensions, trade restrictions, and supply bottlenecks drive diversification efforts. |

Future Outlook | Investments in advanced packaging and materials innovation continue; reshoring ongoing but East Asia remains critical. |

Note: Achieving full self-sufficiency requires massive investment and increases costs, making regional diversification a complex but necessary strategy.

Talent & Workforce

Talent shortages present a major challenge for the Semiconductor Supply Chain. Over one million skilled workers will be needed globally by 2030. The U.S. alone faces a gap of 70,000 workers, with fewer than 100,000 electrical engineering and computer science graduates each year. Rapid technological change demands new skills in AI, robotics, and data analytics. Companies compete with other tech sectors for talent, intensifying recruitment challenges. Aging workforces and high turnover rates add to the problem.

Declining STEM enrollments in key countries reduce the talent pool.

One-third of U.S. semiconductor employees are 55 or older and nearing retirement.

Skills in AI and machine learning now surpass traditional design expertise.

High turnover rates stem from limited career development and workplace flexibility.

Geographic concentration of manufacturing limits workforce growth in new regions.

Companies and governments address these challenges by developing strategic workforce plans, investing in training, and collaborating with educational institutions. The CHIPS Act funds STEM scholarships and workforce programs. Partnerships with universities and technical schools expand talent pipelines. Continuous learning and reskilling programs keep workers updated with new technologies. Diversity and inclusion initiatives attract a broader talent pool.

Regulatory Shifts

Recent regulatory changes reshape the Semiconductor Supply Chain. Environmental regulations such as REACH, RoHS, and WEEE increase compliance requirements and production costs. Companies must reformulate materials and enhance testing to meet these standards. U.S.-China trade tensions result in export controls, tariffs, and trade restrictions, disrupting supply chains and forcing companies to reconsider sourcing strategies. Taiwan’s expanded trade blacklist aligns with U.S. policies, restricting business with Chinese firms and impacting China’s semiconductor ambitions.

U.S. tariffs and retaliatory measures by China and the EU cause companies to rethink global sourcing and manufacturing.

The CHIPS Act accelerates domestic investments and reduces reliance on Asian suppliers.

Companies diversify supplier networks to include allied countries like Taiwan and South Korea.

Tariffs and trade policies shift the industry toward nationalized, protectionist approaches.

Strategic partnerships and joint ventures help navigate the evolving trade environment.

Tip: Companies that adapt through diversification and domestic investment gain competitive advantages in a complex regulatory landscape.

The Semiconductor Supply Chain continues to evolve through innovation, regional investment, and proactive risk management. Companies can build resilience by diversifying suppliers, investing in local production, and collaborating across sectors.

Incentives, workforce development, and digital transformation drive competitiveness.

Joint ventures and government partnerships help secure critical materials and talent.

Data-driven strategies and sustainability practices turn complexity into opportunity.

Proactive adaptation and cross-regional collaboration will shape a secure and innovative future for the industry.

FAQ

What drives growth in the semiconductor supply chain?

AI, automotive technology, and cloud computing push demand higher. Companies invest in new factories and advanced equipment. Government incentives, like the CHIPS Act, support expansion.

These factors help the industry reach new markets and increase production.

How do companies manage supply chain risks?

Companies use multiple suppliers and regions. They keep extra inventory and work closely with partners.

AI tools help spot problems early.

Strong cybersecurity protects against attacks.

Why is regional diversification important?

Regional diversification reduces risk from natural disasters or political issues.

Companies build factories in different countries. This strategy keeps production stable and protects against supply chain disruptions.

What are the main sustainability challenges?

Semiconductor manufacturing uses a lot of energy and water.

Challenge | Impact |

|---|---|

High energy use | Increases costs |

Water demand | Strains resources |

Rare materials | Raises concerns |

How does talent shortage affect the industry?

A lack of skilled workers slows innovation and factory growth.

Companies invest in training and partner with schools. They need more engineers and technicians to keep up with new technology.

See Also

How IoT Is Transforming The Supply Chain Landscape

Career Opportunities Within The Future Supply Chain Industry

Top Five Trends Driving Supply Chain Efficiency Forward